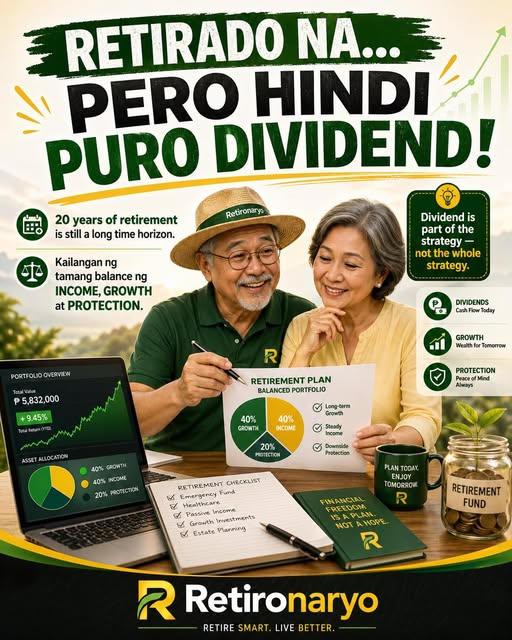

I don’t think I will ever be a pure dividend investor, even when I retire at 60 — at least not 100%.

- retironaryo

- Apr 26

- 2 min read

Updated: May 6

Kung ang life expectancy ko ay 80 years old, that means I still have around 20 years of life after retirement. That is 20 years without active employment income, relying mostly on the retirement fund that Mimi and I were able to build.

These are my reasons:

1) We started late in building our retirement fund.

Just like many people, hindi kami nagsimula nang maaga. Based on the projected retirement fund we may have by the time we retire, it may not be big enough to produce dividends that can fully finance the lifestyle we want.

Kaya kung dividends lang ang aasahan, baka kulang. We still need growth.

2) Retirement does not mean doing nothing.

When we retire, we will probably have more time. Instead of doing nothing, I might as well spend part of that time doing what I do best — studying great companies, looking for good investment opportunities, and managing our portfolio properly.

Of course, I will need to adjust our asset allocation to make sure we are not too exposed to market downturns during retirement. Hindi na pwedeng puro aggressive. But it also does not mean everything must become too conservative.

3) Twenty years is still a long investment horizon.

Many people think that once you retire, dapat puro conservative investments na lang or dividend stocks. But 20 years is still a long time.

For me, that is still enough time to let part of the portfolio continue growing. I still want to take advantage of compounding so the fund can last longer, grow further, and help finance a better retirement lifestyle.

4) If we do not use everything, our children can inherit the portfolio.

If Mimi and I die earlier than expected, then the remaining investments can be passed on to our children. That is not a bad outcome. It becomes part of the legacy we leave behind.

So for me, retirement investing is not simply about dividends.

It is about balance.

Some income.

Some growth.

Some protection.

Some cash buffer.

And a clear plan on how to withdraw money without destroying the portfolio too early.

I may use dividend stocks as part of the strategy, but I do not think I will rely on dividends alone.

Because retirement is not just about surviving.

It is about living well, protecting the fund, and still allowing the money to grow.

Comments