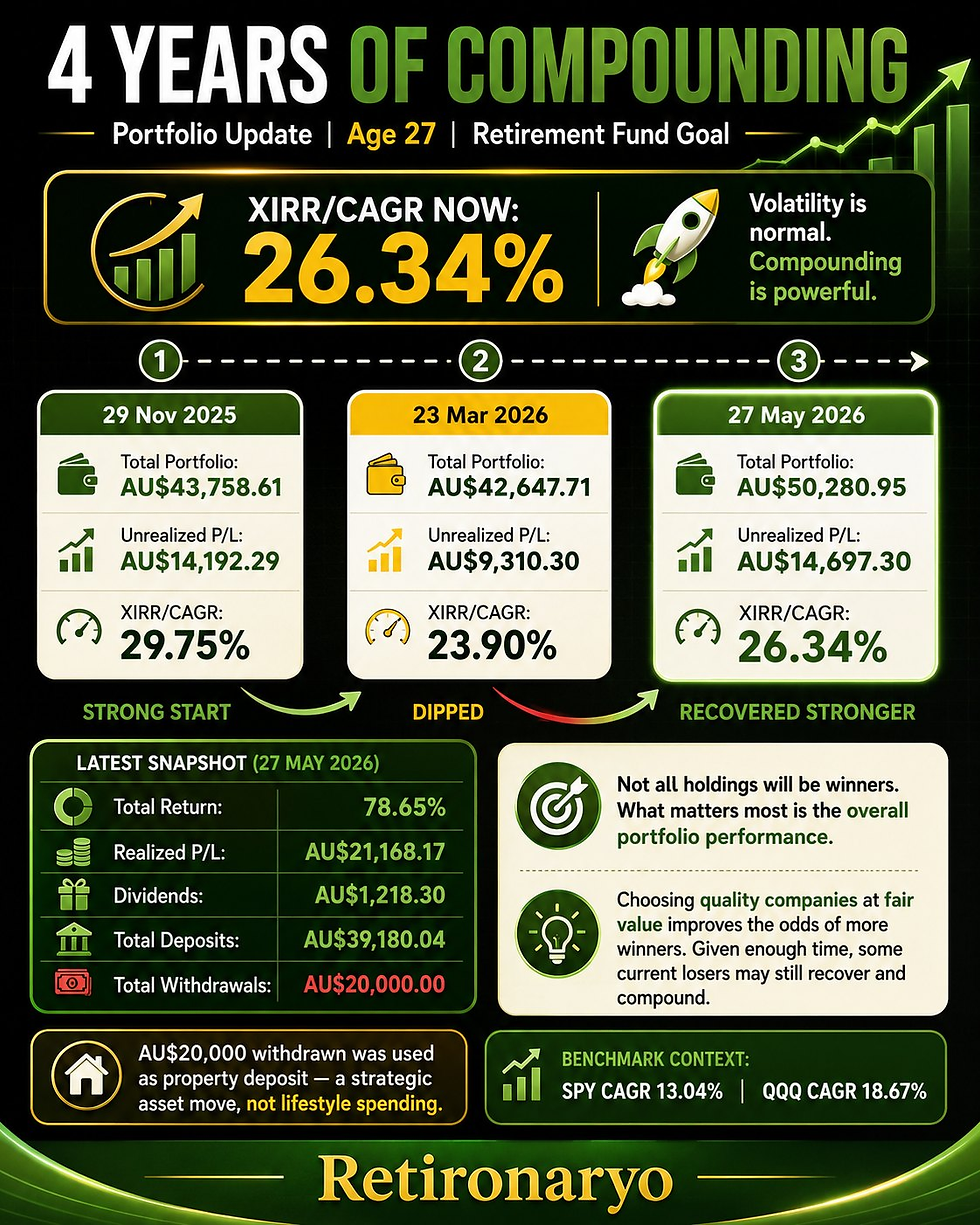

KAYA AYAW MO BANG MAG-INVEST SA S&P 500 DAHIL MALAKI ANG TAX NG USA?

- retironaryo

- Apr 26

- 3 min read

Updated: May 6

May mga nagsasabi:

“Malaki ang tax sa US.”

“25% ang tax kapag hindi ka US citizen.”

“May bank charges pa.”

“Kaya baka hindi rin sulit mag-invest sa S&P 500.”

Valid concern. Pero kailangan linawin.

Hindi 25% tax sa buong investment mo.

Hindi rin 25% tax sa buong profit mo.

Kung direct kang bumili ng US ETF like S&P 500 ETF, ang US withholding tax ay karaniwang applicable sa dividends, hindi sa buong growth ng investment. For Philippine residents, the US treaty dividend rate is generally 25%, provided the proper treaty documentation such as W-8BEN is in place. Without proper documentation, the default US withholding on certain US-source income can generally be 30%.

Halimbawa, kung ang S&P 500 ETF ay may dividend yield na around 1.5% per year, ang 25% tax ay hindi 25% ng buong portfolio. It is 25% of the dividend only.

So kung 1.5% ang dividend yield, 25% tax on that is around 0.375% per year na tax drag.

Masakit? Yes.

Nakakabawas? Yes.

Pero ibig sabihin ba hindi na worth it ang S&P 500? Not necessarily.

Kasi ang malaking bahagi ng return ng S&P 500 ay hindi lang galing sa dividends. Malaking bahagi nito ay galing sa capital appreciation, or pagtaas ng value ng companies over time.

For many non-US investors, US capital gains tax generally does not apply unless certain conditions are met, such as being present in the US for 183 days or more during the taxable year and having US-source capital gains under specific rules.

Kaya mali ang mindset na:

“May 25% tax sa US, kaya lugi na agad.”

Ang mas tamang tanong:

“After tax, fees, and bank charges, mas mataas pa rin ba ang net total return compared sa alternatives ko?”

Now compare natin sa UITF.

Kung ayaw mo or hindi ka makapag-direct invest sa US ETF, puwede kang gumamit ng Philippine UITF na exposed sa S&P 500. Mas convenient ito because local bank ang kausap mo, peso account ang gamit mo, at mas simple para sa maraming Filipino investors.

Pero hindi ibig sabihin nito ay walang cost.

For example, BPI US Equity Index Feeder Fund aims to track the S&P 500 Net Total Return Index before fees and expenses, invests through a target fund such as SPDR S&P 500 ETF Trust, and has a trust fee of 1.50% per year for its listed classes. Its NAV is computed net of taxes, fees, and qualified expenses.

Under recent Philippine tax updates, gains from redemption of UITFs and mutual funds may be exempt if taxes were already withheld at the asset level. But again, that does not mean zero cost. It means many of the taxes and expenses are already reflected in the NAVPU.

So ganito ang practical comparison:

Direct US ETF investing:

Mas mababa usually ang management fee. Mas may control ka. Pero may US dividend withholding tax, possible bank transfer fees, FX conversion cost, platform risk, tax reporting responsibility, and estate tax concern.

S&P 500 UITF:

Mas convenient. Local bank. Mas simple for many Filipinos. Pero usually mas mataas ang annual trust fee, less control, and the taxes/expenses are already embedded in the NAVPU.

Kaya hindi dapat tax lang ang tinitingnan.

Ang dapat tingnan ay:

Net total return after taxes, fees, FX cost, and convenience.

Kahit may US dividend withholding tax, kung ang long-term net return ng S&P 500 exposure ay mas mataas pa rin kaysa sa ibang available options mo, then it may still be a good retirement-building vehicle.

Huwag nating gawing dahilan ang tax para manatili sa investment na hindi naman kayang abutin ang retirement goal natin.

Yes, taxes matter.

Fees matter.

Bank charges matter.

Pero mas mahalaga pa rin ang tanong:

After all costs, alin ang may mas mataas na chance na maabot ang retirement fund na kailangan mo?

Kasi sa retirement planning, hindi sapat ang “mababa ang tax.”

Ang importante ay sapat ang magiging retirement fund mo.

Know your numbers.

Compare net returns.

Then choose the investment vehicle that gives you the best chance of reaching your goal.

Hindi porket may tax, hindi na sulit.

Mas delikado kung dahil sa takot sa tax, hindi mo naabot ang retirement fund na kailangan mo.

Comments