Portfolio #1 Update as of 25 Oct 2025

- retironaryo

- Oct 24, 2025

- 2 min read

I asked ChatGPT to analyze this portfolio and this is the response and recommendations.

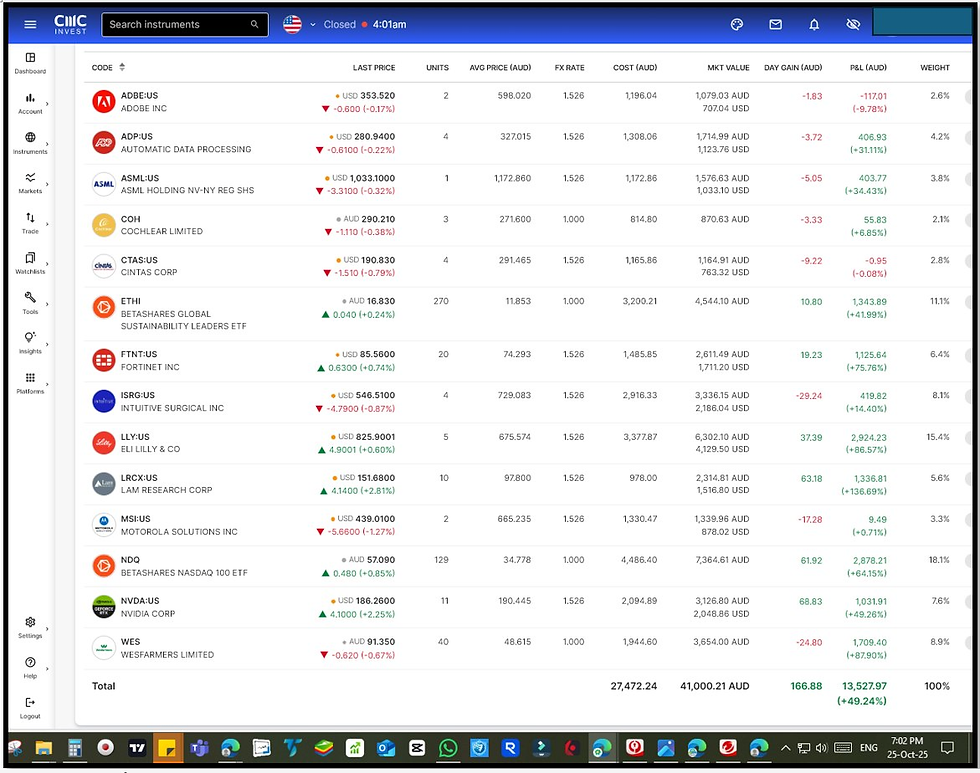

Snapshot (25-Oct-2025)

Age 3.59 yrs | Total A$42,004.69 (Holdings A$41,000.21 + Cash A$1,004.48)

Net deposits A$12,255.10 | Cost basis A$27,472.24

Unrealized +A$13,527.97 (+49.24%) | Realized +A$21,168.17 | Dividends A$1,045.87

Total return vs net deposits ~+87.2% | XIRR ~30.07%

Benchmarks since start: SPY ~12.1%, QQQ ~16.5%

Recent activity (Jul–Oct 2025)

31 Jul: Closed META at +315.06% profit (CAGR ~53.88%).

21 Aug: Closed FAST at +108.33% profit (CAGR ~26.99%).

26 Aug: Opened ASML.

05 Sep: Added ISRG.

21 Oct: Bought CTAS.

Positioning & drift

Biggest weights: NDQ (18.1%), LLY (15.4%), WES (8.9%), ISRG (8.1%), NVDA (7.6%), ETHI (11.1%).

Tech remains the dominant bet (NDQ + NVDA/ASML/LRCX/FTNT/ADBE/MSI). Health-care tilt via LLY / ISRG / COH; AU ballast via WES, ETHI. Cash ~2.4%.

What the trades say (and what to do next)

Excellent profit harvesting.

Exiting META (+315%) and FAST (+108%) crystallized large wins and reduced single-name risk. Keep a standing rule: trim/exit when a name breaches max weight or hits your valuation band—you executed this well.

Thoughtful redeploy.

Rotating proceeds into ASML (semicap leader), ISRG (procedural growth), and CTAS (steady B2B services) adds quality and slightly broadens sector exposure. Guardrails: ≤15% per stock, ≤20% per ETF; ≤60% tech exposure.

Cyclical-valuation watch.

With ASML / LRCX / NVDA, earnings are powerful but semi cycles can compress multiples fast. Set buy/add/trim bands now; consider a staggered add plan on 15–20% pullbacks.

Core–satellite clarity.

Treat NDQ + ETHI as core (30–45%); satellites are your moat names (LLY, ISRG, NVDA, ASML, LRCX, FTNT, WES, CTAS). Rebalance quarterly or on ±25% drift from target weights.

Laggards decision.

Re-underwrite ADBE / MSI / COH / CTAS (new): confirm moat trajectory, FCF durability, and 3–5y IRR. If thesis < your hurdle, recycle capital to higher-conviction names or core.

Liquidity & FX.

Cash is lean at ~2.4%. If you expect volatility, lift to 5–8% or run a small DCA into core. Note AUD/USD will keep adding noise—acceptable if liabilities are in AUD and you want USD diversification.

Planning realism.

Your ~30% XIRR is outstanding but not a planning baseline. Use 8–12% for long-term projections; treat excess as upside.

Comments